Form 926: Step-by-Step Guide for Accurate Filing

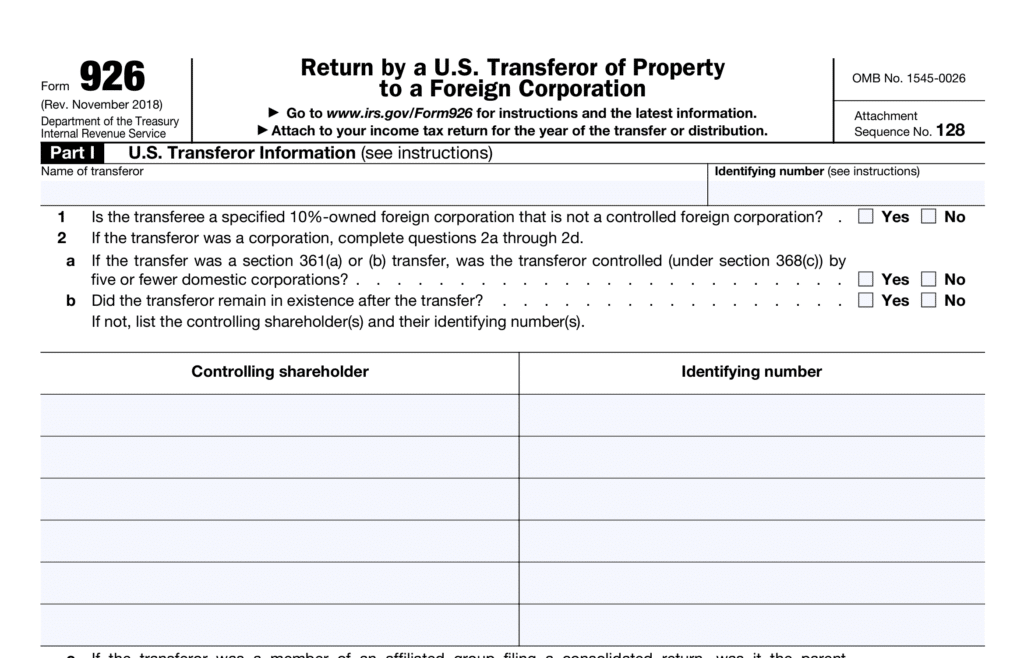

- What Is Form 926?

- Who Files Form 926?

- Transfers of Cash or Stock/Securities: When to File Form 926

- Distributions by Domestic Liquidating Corporations

- Form 926 Filing Deadline

- Form 926 Exceptions (Who Does Not Have to File it?)

- Penalties for Failure to File Form 926

- Avoiding IRS Failure to File Penalties

- Get Help With Form 926 from Greenback

Key Takeaways

- US persons use Form 926 to report the transfer of cash or property to a foreign corporation.

- This form may be required for US citizens, residents, and various business entities.

- Failing to file Form 926 when required can result in substantial penalties, but there are ways to reduce or avoid these penalties if you act quickly.

What Is Form 926?

IRS Form 926 is used to report the exchange or transfer of property to a foreign corporation. This includes:

- US persons transferring cash or property to a foreign corporation.

- US persons exchanging cash or property for a controlling share in a foreign corporation.

Who Files Form 926?

The “US persons” who must file Form 926 means more than just an individual person. In the eyes of the IRS, a US person can include any of the following:

- US citizen

- US resident

- Domestic corporation

- Domestic estate

- Domestic trust

- Domestic partnership

Do you know how the IRS taxes Kabushiki gaisha taxes? Check it out!

Transfers of Cash or Stock/Securities: When to File Form 926

Simply transferring cash to a foreign corporation does not necessarily mean you have to file Form 926. You are only required to file Form 926 if either of the following is true:

- You own 10% or more of the foreign corporation after the transfer.

- You transfer more than $100,000 over a 12-month period.

Any transfer of stock or securities to a foreign corporation must be reported on Form 926.

Distributions by Domestic Liquidating Corporations

If a domestic corporation is in the process of liquidation and distributes its assets to a foreign corporation, it may be required to file Form 926 to report this. The rules for when this is required are complex. To learn more, review the instructions provided by the IRS or consult a qualified tax professional.

Form 926 Filing Deadline

Form 926 should be attached to your annual tax return and filed by the same deadline as your annual tax return.

Form 926 Exceptions (Who Does Not Have to File it?)

In some cases, a person may be exempt from filing Form 926.

1. Exchanges of Stock or Boot

If a transaction involves stock and boot, it may be exempt from File 926 reporting under specific conditions. This exemption recognizes that not all transactions pose the same level of risk or need for scrutiny. Whenever there is an exchange of one type of stock for another type of stock plus cash or other property, the cash or other property is boot.

2. LESS Than 5% Voting and Total Value AND…

Minor stakeholders in a foreign corporation can also be exempt from filing Form 926. This applies if the US person owns LESS than 5% of voting power and total value in the corporation. Other conditions must be met as well. For example, at least one of the following must be true:

- The transfer didn’t have to be taxed because of specific tax rules (nonrecognition treatment).

- The person or organization making the transfer doesn’t pay taxes on this type of income (for example, a charity), and this transfer doesn’t change that.

- The transfer was supposed to be taxed, and the person did report and pay taxes on it correctly during tax filing.

- The transfer is only considered as going to a foreign company due to specific rules, and the total value of what was transferred is less than $100,000.

This exemption simplifies the filing process for individuals and entities with minimal foreign investments.

3. MORE than 5% Voting and Total Value AND…

If the US person owns MORE than 5% in both voting rights and total value in a foreign corporation does not need to file Form 926 if any of the following is also true:

- The US transferor is an organization that doesn’t have to pay taxes (like charities) and the money made from the transfer isn’t from a business activity unrelated to their main purpose.

- The transfer resulted in income that the US transferor had to pay taxes on, and they reported this income correctly and on time on their tax return.

- The only reason the transfer counts as going to a foreign corporation is because of a specific rule (Regulations section 1.83-6(d)(1)), and the value of what was transferred is less than $100,000.

The exceptions to filing Form 926 are nothing if not complex. If you believe you’re exempt from filing, review the specific conditions closely. Misunderstanding these exemptions can lead to unintentional non-compliance.

Penalties for Failure to File Form 926

Failing to file Form 926 when required can result in severe consequences. Penalties include 10% of the value of the transfer, with a maximum of $100,000 per incident. However, if the failure to file was due to reasonable cause, this penalty can be waived.

On the other hand, if the failure to file was due to willful disregard of the rules, the $100,000-per-incident cap is removed, and penalties can be even more severe. In extreme cases, this could result in criminal charges for tax evasion.

Avoiding IRS Failure to File Penalties

If you have failed to file Form 926 (or any other tax form), the IRS offers various tax amnesty programs that can allow you to come into compliance without facing the usual penalties. To use these programs, your failure to file must have been accidental, and you must come forward voluntarily. If the IRS contacts you about your delinquency first, you may lose the right to amnesty.

Keep detailed records of all your international transfers, including the nature of the property transferred, the foreign corporation that received the transfer, and the terms of the transaction. This documentation will be invaluable if the IRS has questions or if you need to prove your compliance.

Get Help With Form 926 from Greenback

Greenback Expat Tax Services specializes in helping Americans around the world meet their US tax obligations. Contact us, and we can file Form 926 (as well as any other form!) on your behalf.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.