Form 3520 for Americans Living Abroad: The Basics

- Do I Need to File IRS Form 3520?

- Do I Need to File Form 3520-A?

- When Does a Reporting Requirement Arise for Americans Living Abroad? (Form 3520 Instructions)

- What Exceptions Should Americans Living Abroad Know About Form 3520-A?

- What Are the Penalties for Not Filing Form 3520?

- US Trusts vs. Foreign Trusts

- Form 3520 and Foreign Trust Reporting

- Filing Form 3520 Doesn't Have to Be Complicated

When certain foreign trust, foreign gift, or foreign bequest transactions occur, the IRS requires Form 3520 to be filed to report such transactions. Form 3520 is a US income tax return form used to report foreign financial assets and transactions. It’s not as simple as it sounds, though, because many different types of information must be reported on the form.

But don’t be intimidated: we’ve broken the information down into a simple guide for Americans living abroad – complete with Form 3520 examples!

Key Takeaways

- Form 3520 is a tax form used to report certain transactions involving foreign trusts.

- Many Americans who interact with a foreign trust are required to file Form 3520.

- Most taxpayers who file Form 3520 will also have to file Form 3520-A.

Do I Need to File IRS Form 3520?

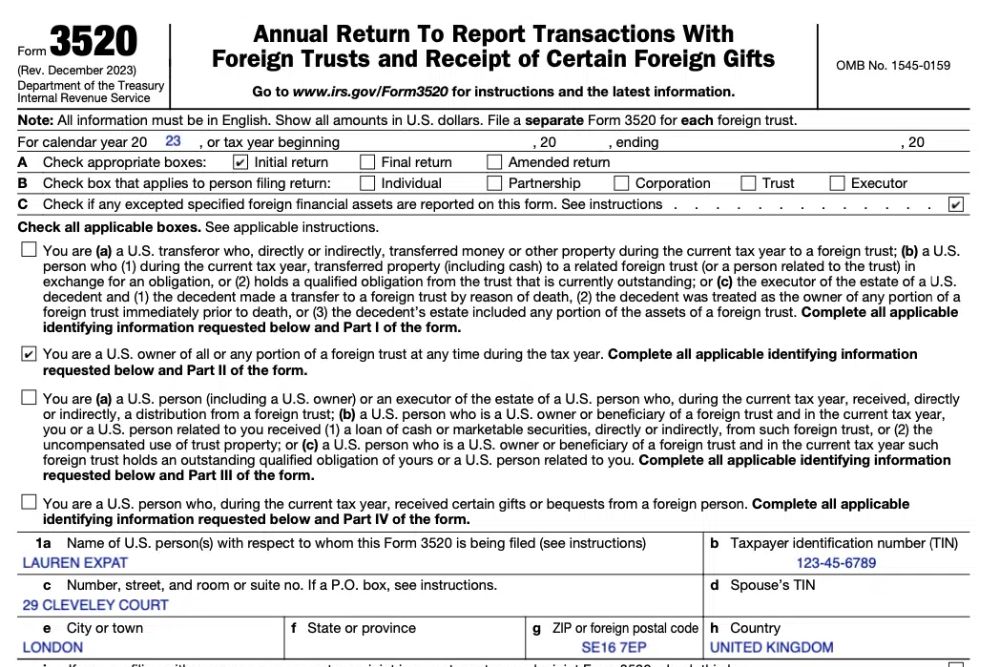

Form 3520 is a tax form that US expats must file if they own foreign trusts, make certain transactions with foreign trusts, or receive large gifts or inheritances from certain overseas persons.

The following situations will trigger a requirement for Americans living abroad to file IRS Form 3520:

- You are the responsible party (grantor with inter vivos trust, transferor other than because of death with a reportable event, executor of the decedent’s estate) for reporting a reportable event that occurred during the current tax year. A reportable event arises when:

- A foreign trust is created by a US person

- Property or money is transferred to a foreign trust by a US person, including:

- Transfers by reason of death

- Transfers applicable to a foreign grantor who later becomes a US person (Sec 679(a)(4)

- Transfers by US citizens/US residents to trusts which were not initially foreign trusts, but subsequently become foreign trusts while the individual is alive (Sec 679(a)(5)

- You are a US person who transferred property (including cash) to a related foreign trust (or a person related to the trust) in exchange for an obligation.

- You are a US person who, during the current tax year, is treated as the owner of any part of the assets of a foreign trust under the rules of sections 671 through 679. Interested in the grantor trust rules? Sections 671-679 cover that.

- You are a US person who received a distribution from a foreign trust during the current tax year.

- You are a US person who is a US owner or beneficiary of a foreign trust, and either you or a US person related to you received a loan or uncompensated use of trust property. And, don’t forget: the loan can be in cash or marketable securities.

- You are a US person who, during the current tax year, received either:

- More than $100,000 from a nonresident alien individual or a foreign estate (including foreign persons related to that nonresident alien individual or foreign estate) that you treated as gifts or bequests; or

- You received more than $18,567 from a foreign company during 2024 that you treated as gifts. This amount usually increases slightly each year to adjust for inflation.

The IRS generally considers retirement plans to be trusts. Many foreign retirement plans are non-qualified plans, and can also be classified as foreign trusts subject to Form 3520 reporting

Do I Need to File Form 3520-A?

In many cases, the filing of Form 3520-A will go hand in hand with Form 3520. Form 3520-A is needed if a foreign trust exists with a US owner. The foreign trust must furnish the required annual statements.

If the foreign trust can’t or won’t file Form 3520-A, is it the responsibility of the US owner or beneficiary to complete and attach it to its Form 3520? This Form 3520-A is technically known as a Substitute Form 3520-A.

When Does a Reporting Requirement Arise for Americans Living Abroad? (Form 3520 Instructions)

Check out these examples to know how the requirements are triggered and more about Form 3520 instructions.

Form 3520 Example #1

Alex, a US citizen, lives in Kansas with his parents. His grandfather (not a US citizen or resident) lives in Spain and wants to give Alex $15,000. His grandfather has a foreign grantor trust, and the trustee accordingly sends Alex $15,000 from the trust.

- Is Form 3520 needed? Yes, Alex is a US person who received a distribution from a foreign trust and must file Form 3520, page one, and Part III to report this distribution.

- Is Form 3520-A needed? Yes, as a US beneficiary of a foreign trust, Alex must ensure that he attaches his Foreign Grantor Trust Beneficiary Statement (page five of Form 3520-A) to his Form 3520.

Form 3520 Example #2

Alex, a US citizen, lives in Kansas with his parents. His grandfather (not a US citizen or resident) lives in Spain and wants to give Alex $15,000. The grandfather decides to write a check to Alex from his personal savings account held in Spain.

- Is Form 3520 needed? No, Alex did not receive a distribution from a trust; it was a gift from a nonresident alien that is less than $100,000. There is no reporting requirement for Form 3520.

- Is Form 3520-A needed? No. Alex is not the owner of a foreign trust and has not received any distributions from it, so Form 3520-A is not applicable.

Form 3520 Example #3

Marina, a US citizen, lives in Germany and has opened a private pension plan. Marina makes all contributions to the plan; it is managed by a trustee who takes title to the property to conserve the funds for Marina, the beneficiary. The trust is protected from creditors. Upon analysis, the trust is deemed to qualify as a foreign grantor trust.

- Is Form 3520 needed? Yes, Marina is a US person and satisfies the ownership rules of a foreign trust. She has also transferred cash/money to the foreign trust.

- Is Form 3520-A needed? Yes, as the US owner of a foreign grantor trust, Form 3520-A must be filed.

What Exceptions Should Americans Living Abroad Know About Form 3520-A?

There are two exceptions to the requirement to file Form 3520-A in the following cases:

- If a foreign trust is considered an employee benefit plan under Sec 402(b), 404(a)(4), or (404A), Revenue Procedure 2020-17 helps clarify the specific requirements that need to be met to qualify as such.

- Custodians of Canadian RRSPs (registered retirement savings plans), Canadian RRIFs (Canadian registered retirement income funds), or custodians of any other Canadian retirement plan that qualify under section 3 of Rev. Proc. 2014-55 are not required to file Form 3520-A for a US citizen or resident alien owner or beneficiary.

What Are the Penalties for Not Filing Form 3520?

Penalties for failing to file Form 3520 as required can be quite severe.

- Failure to file a timely Form 3520-A, failure to file all information, or filing includes incorrect information: The initial penalty is the greater of $10,000 or 5% of the gross value of the portion of the trust’s assets treated as owned by the US person at the close of the tax year.

- Failure to file a timely Form 3520 (Part II), failure to furnish all information required, furnishes incorrect information: This additional separate penalty is the greater of $10,000 or 5% of the gross value of the portion of the trust’s assets treated as owned by the U.S. person at the close of that tax year.

- Failure to report the creation or transfer to a foreign trust: 35% of the gross value of any property transferred to a foreign trust.

- Failure to report distributions received from a foreign trust by a US person: 35% of the gross value of the distributions.

The deadlines for these two forms are different! Form 3520 follows the regular schedule of IRS tax return deadlines and is due April 15 , with expats receiving an automatic two-month extension through June 15 (June 16 in 2025, since June 15 falls on a weekend) .

Form 3520-A is due on March 15, so this will be yet another deadline to tuck into your file of important expat tax information!

If you have to file either of these forms, you should always file a regular extension on form 4868 which could help you to avoid penalties by not filing forms 3520 and 3520-A on time.

US Trusts vs. Foreign Trusts

When it comes to reporting a trust on your US Tax Return, you must know the difference between a US trust and a foreign trust, as the reporting requirements differ for each.

- US Trust: You will use Form 1041 and will check the ‘grantor trust’ box in the upper left corner.

- Foreign Trust: You will use Form 1040NR and will check the ‘estate or trust’ box in the upper right-hand corner. If the grantor is an individual, he or she will need to check the box on Schedule B, Part III, line 8 of Form 1040 each year to report the foreign trust.

The typical asset protection trust will be classified as a ‘grantor trust’ while the settlor is living. This means the grantor will report and pay all US taxes reported by the trust, including interest, dividends, and capital gains.

The IRS avoids using ‘offshore trust’ to differentiate these two, because ‘offshore’ could technically be a US or foreign trust – so the key difference between the two is in how you file them.

Form 3520 and Foreign Trust Reporting

If the failure to report is due to reasonable cause and not due to willful neglect, the penalties above can be abated for foreign trust reporting. On the positive side, both Forms 3520 and 3520-A are informational returns that typically don’t have taxes due with the filing of the forms. However, as we mentioned above, penalties can be significant for non-compliance.

Filing Form 3520 Doesn’t Have to Be Complicated

Expat taxes can be complex, but we can help you file your Form 3520. Our team of tax professionals specializes in expat taxes, so we can ensure you rest easy.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.