Form 709: Guide to US Gift Taxes for Expats

- What Is Form 709?

- What Is the US Gift Tax?

- What Qualifies as a Taxable Gift?

- What Types of Gifts Are Tax-Exempt?

- Who Files Form 709?

- Will I Owe Taxes When I File Form 709?

- How Does the US Gift Tax Apply to Non-US Persons?

- When Is Form 709 Due?

- What Happens If I Don’t File Form 709 on Time?

- How Do I File Form 709?

- Key Changes to Form 709 for the 2024 Tax Year

- Have Questions about Form 709? Get the Answers You Need!

If you’ve given someone a gift worth more than $18,000 in 2024, you probably need to file IRS Form 709 for the 2024 tax year (Filed in 2025). This form can be complicated—especially for expats. Fortunately, we’re here to clear things up.

In this guide, we’ll take a look at what expats need to know about Form 709 and the US gift tax. Let’s get started!

Key Takeaways

- When a US person transfers cash or property to another person without asking for anything in return, it is considered a gift. If this gift meets certain criteria, it is subject to US gift tax and must be reported on Form 709.

- The US gift tax applies to the person who gives the gift, not the one who receives it.

What Is Form 709?

Form 709 is an IRS form used to report certain taxable gifts. If a taxpayer gives a gift that is subject to the US gift tax, they must fill out Form 709 and file it by the appropriate deadline.

What Is the US Gift Tax?

When a US person transfers cash or property to another person without requiring payment in return, that is considered a gift. If that gift meets certain conditions, it will be subject to the US gift tax and must be reported using Form 709.

What Qualifies as a Taxable Gift?

The IRS defines a gift as virtually anything of value that a US person gives to someone else without being paid in return. This includes transfers in the form of:

- Cash

- Financial accounts, such as stocks

- Tangible property, such as a house, car, or jewelry

- Forgiven debts

- Interest-free loans

Not all gifts are taxable under the US gift tax, however. Only gifts that exceed the annual gift tax exemption must be reported. For the 2024 tax year (Filed in 2025), the annual gift tax exemption is $18,000. This is the amount you can gift to another person without triggering the US gift tax. If you exceed this amount, your gift will become taxable and must be reported. This is true regardless of whether you exceed the threshold with a single gift or multiple gifts given to the same person.

For example, let’s say you gave your son a car worth $20,000 at the start of this year. Because this gift exceeds the $18,000 threshold, you would need to report it as a taxable gift. If you instead gave your son a cash gift of $10,000 in January and then a second cash gift of $9,000 in August, this would also qualify as a taxable gift since the two amounts exceed the annual gift tax exemption.

However, the annual gift tax exemption applies only to gifts given to a single person. If you give more than $17,000 to multiple people but never more than $18,000 to any one person, those gifts will not be taxable.

The 2024 annual gift tax exemption for married couples filing jointly doubles to $36,000.

What Types of Gifts Are Tax-Exempt?

Not all gifts are subject to the US gift tax, even if they exceed the annual gift tax exemption. In most cases, you will not have to file Form 709 for these types of gifts:

- Payment of medical expenses

- Payment of tuition for an educational institution

- Gifts to a political organization

- Gifts to your spouse (this only applies if your spouse is a US person—if they are not, your gift may not be exempt)

You can deduct gifts given to qualifying charities when filing your tax return if you itemize your deductions instead of taking the standard deduction.

Who Files Form 709?

The US gift tax applies to the person who gives the gift, not the one who receives it. This means that if you give away a taxable gift, you must report it using Form 709. If you are the recipient of a taxable gift, however, you do not have to file this form.

Will I Owe Taxes When I File Form 709?

For most taxpayers, Form 709 is an informational tax form and does not result in immediate tax liability. This is because all US persons have a lifetime gift tax exemption of $13.61 million in 2024.

Even if you exceed the annual gift tax exclusion and are required to file Form 709, you will not owe taxes until your total lifetime gifts exceed $13.61 million. Once you surpass this threshold, any additional gifts will be subject to gift tax, which is generally taxed at a 40% rate.

The lifetime gift tax exemption is set to drop significantly in 2026, reverting to $5 million (adjusted for inflation) unless new legislation is enacted. This means taxpayers making large gifts may want to consider planning before the exemption decreases.

How Does the US Gift Tax Apply to Non-US Persons?

Does the US gift tax apply when a foreign person is involved in the transaction? The answer depends on who gives the gift.

- If a US person gives a taxable gift to another person, the US person must always file Form 709. It does not matter whether the recipient is a US person or not.

- If a foreign person gives a gift of any amount to a US person, the foreign person will probably not have to file Form 709. (The only exception to this is if the gift is a tangible property located in the US, such as a house.)

In either case, the recipient is never required to file Form 709.

If a foreign person gives a gift of $100,000 or more to a US person in a single year, the US recipient may be required to report the gift on Form 3520.

The reporting threshold is much lower for gifts made through a foreign entity. If a foreign company or trust gives a gift to a US person, the Form 3520 filing requirement is triggered at approximately $19,570 in 2024 (adjusted annually for inflation).

When Is Form 709 Due?

The deadline for Form 709 is the same as the due date for your US tax return. In most years, this would be April 15

What Happens If I Don’t File Form 709 on Time?

Failing to file Form 3520 when required can result in severe penalties—typically up to 25% of the total gift amount received. To avoid these penalties, US recipients of large foreign gifts should ensure timely and accurate reporting.

How Do I File Form 709?

If you need to file Form 709, follow these steps:

- Gather any information you’ll need to complete the form, such as documents relating to a gift.

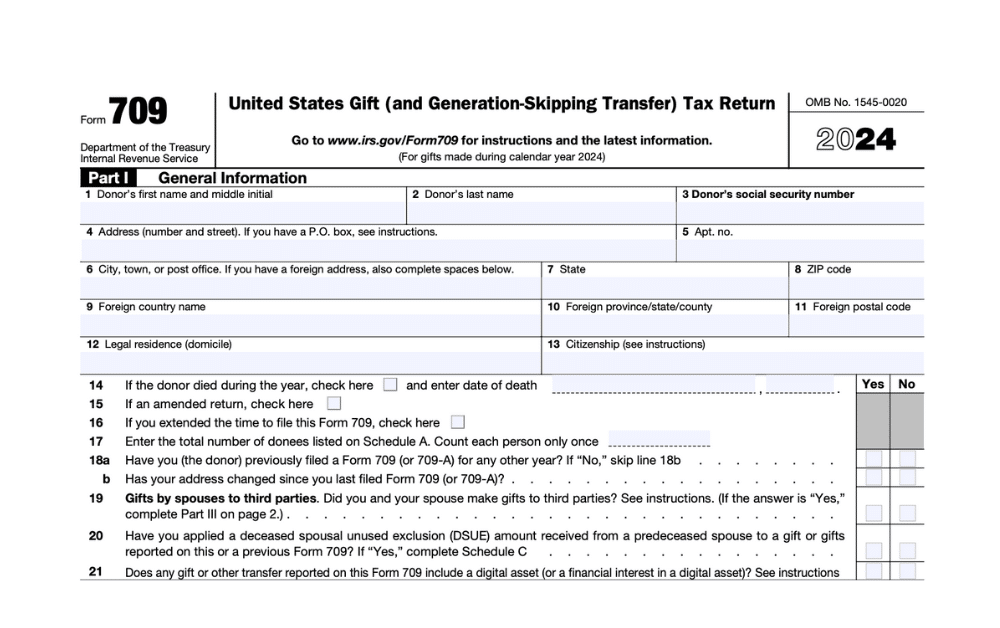

- Fill out Form 709 on the IRS website. The form is a five-page document with sections covering your personal information and details of any taxable gifts you made. Depending on what you’re reporting, you may not have to complete every section.

- Download your completed form and print it. (You cannot e-file Form 709.)

- Please mail Form 709 to the IRS at their service center in Kansas City, Missouri, before the annual deadline.

Once your form is in the mail, you’re all set.

If you need more time to prepare your Form 709, you can file for an extension using IRS Form 8892. This will give you an automatic six-month extension, extending the deadline to October 15. However, if you file Form 4868 for an extension for your annual tax return, you will also have an automatic extension for Form 709. You will not have to file a separate Form 8892.

For more details on how to file Form 709, see the Form 709 instructions on the IRS website.

Form 709 is an incredibly complicated tax form. We recommend always consulting a qualified tax professional before attempting to file this form independently.

Key Changes to Form 709 for the 2024 Tax Year

The IRS has introduced several updates to Form 709 (United States Gift and Generation-Skipping Transfer Tax Return) for the 2024 tax year. Below are the key changes:

1. Reorganization of Part I – General Information

- The entry lines in Part I have been reorganized for better clarity.

- The form now includes designated spaces for foreign address entries.

- Lines 12 through 18 have been moved to Part III.

2. New Part III – Spouse’s Consent on Gifts to Third Parties

- Lines 12 through 18 have been relocated and now appear under Part III, which is found on the second page of Form 709.

- A consenting spouse is no longer required to sign the return itself. Instead, they must sign a separate Notice of Consent, which must be attached to the donor’s return.

3. Changes to Schedule A

- The columns for Parts 1, 2, and 3 of Schedule A have been reorganized.

- New columns (k), (l), and (m) have been added, along with checkboxes in Parts 1 and 3, to indicate whether the gift qualifies as:

- A charitable gift,

- A deductible gift to a spouse, or

- A 2652(a)(3) election.

4. Introduction of Form 709-NA for Nonresident Aliens

- Nonresidents who are not US citizens and have made gifts of tangible property located in the United States must now file Form 709-NA instead of Form 709.

5. Annual Gift Exclusion Amounts for 2024

- The annual gift tax exclusion has increased to $18,000 per recipient in 2024.

- For gifts made to spouses who are not US citizens, the annual exclusion has increased to $185,000.

6. Gift and Generation-Skipping Transfer Tax Rates

- The top tax rate for both gifts and generation-skipping transfers remains at 40%.

7. Basic Credit and Exclusion Amounts for 2024

- The basic credit amount for 2024 is $5,389,800.

- The applicable exclusion amount is $13,610,000 in 2024.

- If a surviving spouse wishes to use any unused exclusion amount from a deceased spouse, the executor of the deceased spouse’s estate must have filed Form 706 in a timely manner to elect portability of the unused exclusion.

Read more about the details of these changes on the IRS site: Instructions for Form 709

Have Questions about Form 709? Get the Answers You Need!

We hope this guide has been helpful and will prove useful to you should you ever have questions about Form 709. If not, we can still assist you with filing your expat tax return—after all, it’s what we do.

Contact us, and one of our customer champions will gladly help. If you need very specific advice on your specific tax situation, you can also click below to get a consultation with one of our expat tax experts.