Form 8938 Filing Requirements & Foreign Asset Reporting

One of the most difficult expat tax forms to understand is Form 8938. For years, this form has been a thorn in the side of American taxpayers around the world. To help clear up this confusing topic, we’ve compiled everything you need to know about IRS Form 8938.

Key Takeaways

- Form 8938 is a mandatory informational tax form for certain US expats and used to report your foreign financial accounts.

- Failing to file Form 8938 when required can result in severe penalties.

What Is Form 8938?

Form 8938 is an informational IRS tax form created as part of the Foreign Account Tax Compliance Act (FATCA), which was passed into law in 2010. The form alerts the IRS that an individual owns certain types of foreign assets.

US persons who own foreign financial assets valued above certain thresholds must file this form to report those assets. Common examples of foreign financial assets include:

- Foreign bank accounts

- Foreign brokerage accounts

- Foreign financial instruments

- Foreign insurance and annuity contracts with cash value

- Shares in foreign hedge funds and private equity funds

- Ownership interests in foreign corporations, partnerships, or LLCs.

This form is required under the rules of the Foreign Account Tax Compliance Act. FATCA is designed to prevent taxpayers from hiding their assets and income overseas to avoid taxation.

While this form is similar to the FBAR, they are not the same. Understanding the differences can be crucial for expat tax compliance.

Get the Free Download That Makes Filing Taxes Simple

Who Has to File this Form?

The threshold for filing Form 8938 depends on your residency and filing status.

For US persons living in the US, the thresholds for filing are:

- Single or Married Filing Separately: You must file Form 8938 if the total value of your foreign assets is greater than $50,000 on the last day of the tax year or more than $75,000 at any point during the year.

- Married Filing Jointly: You must file Form 8938 if the total value of the foreign assets you and your spouse own is greater than $100,000 on the last day of the tax year or more than $150,000 at any point during the year.

For US persons living outside of the US, the thresholds for filing are much higher:

- Single or Married Filing Separately: You must file Form 8938 if the total value of your foreign assets is greater than $200,000 on the last day of the tax year or more than $300,000 at any point during the year.

- Married Filing Jointly: You must file if the total value of the foreign assets you and your spouse own is greater than $400,000 on the last day of the tax year or more than $600,000 at any point during the year.

Refer to the table below for a summary of these rules.

Form 8938 Filing Thresholds

| Single | Married Filing Jointly | Married Filing Separately | |

| Living inside the US | $50,000 on the last day of the year or $75,000 at any point during the year | $100,000 on the last day of the year or $150,000 at any point during the year | $50,000 on the last day of the year or $75,000 at any point during the year |

| Living outside US | $200,000 on the last day of the year or $300,000 at any point during the year | $400,000 on the last day of the year or $600,000 at any point during the year | $200,000 on the last day of the year or $300,000 at any point during the year |

What Are the Penalties for Failing to File this Form?

Failing to file Form 8938 when required can result in severe penalties. The standard penalty is a fine of $10,000 per year. If the IRS notifies taxpayers that they are delinquent, they will have 90 days to comply. Until the taxpayer files the form 8938, they may be fined an additional $10,000 for every 30 days of noncompliance, up to a maximum of $50,000. (This $50,000 maximum does not include the original $10,000 per year.)

On top of this, the IRS says that “underpayments of tax attributable to non-disclosed foreign financial assets will be subject to an additional substantial underpayment penalty of 40%.”

In very rare instances, criminal penalties may also apply. The moral of the story is that you should always file this form when required.

What’s the Difference Between Form 8938 and the FBAR?

Form 8938 and FinCEN Form 114 (commonly known as the Foreign Bank Account Report or FBAR) are both used by US taxpayers to report foreign financial assets, but they have some key differences.

| Details | Form 8938 | FinCEN Form 114 (FBAR) |

| Who Must File: | US citizens, resident aliens, and certain non-resident aliens and specified domestic entities with foreign financial assets exceeding certain thresholds | US persons (citizens, resident aliens, trusts, estates, domestic entities) with one or more foreign financial accounts exceeding $10,000 in aggregate at any time during the calendar year |

| Reportable Assets: | Foreign financial accounts and other foreign non-account assets, such as: Foreign stocks or securities not held in a financial account, Foreign partnership interests, Foreign mutual funds, Foreign hedge funds and private equity funds, Certain foreign-issued life insurance or annuity contracts | Foreign financial accounts and other foreign non-account assets, such as: Foreign stocks or securities not held in a financial account, Foreign partnership interests, Foreign mutual funds, Foreign hedge funds and private equity funds Certain foreign-issued life insurance or annuity contracts |

| Filing Deadline: | Due along with the annual income tax return (including extensions) | April 15, with an automatic extension to October 15 |

| Where to File: | Submitted to the IRS along with your income tax return | Filed electronically through FinCEN’s BSA E-Filing System |

| Penalties: | Up to $10,000 for failure to disclose, with additional penalties up to $50,000 for continued failure after IRS notification; potential criminal penalties | Non-willful violations: up to $10,000 per violation. Willful violations: the greater of $100,000 or 50% of the account balance per violation; potential criminal penalties |

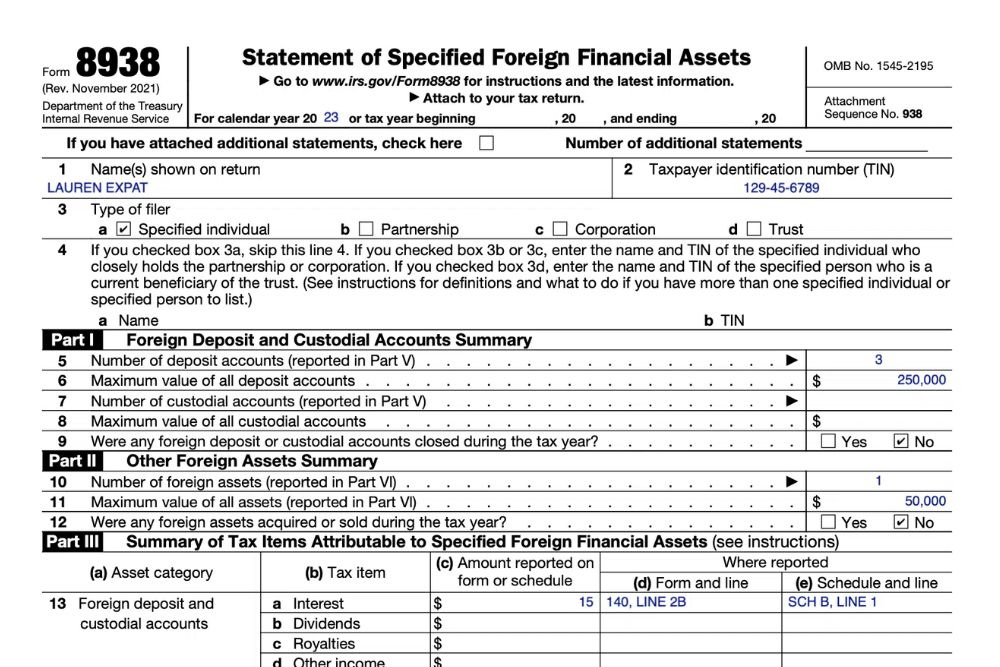

What Information Is Reported on Form 8938?

Form 8938 requires that the filer report information about foreign accounts and assets, including:

- The account number

- The name and address of the financial institution that maintains the account

- The highest value in the account during the year

- The joint account owner’s name, if applicable

You will also list any income earned from each account during that year. This income should match what you report on Schedule B (interest and dividends) of your income tax return.

For more, see the instructions for Form 8938 listed on the IRS website.

Want Help Filing Form 8938? We Can Help!

We hope this guide has helped you understand the requirements and instructions for Form 8938. However, expat taxes are nothing, if not complex. If you still have questions, we have the answers you need. In fact, we can even prepare and file Form 8938 on your behalf.

Have questions about the process or next steps? Contact us, and one of our Customer Champions will happily address all your concerns. If you’re ready to be matched with a Greenback accountant, click the get started button below.